Why Project Profitability Reports Matter

Margins in construction are often tight. A single overlooked cost can turn a profitable job into a financial headache. Yet many contractors still rely on gut feel when reviewing project performance. That’s a mistake.

If you’re using QuickBooks Online but haven’t set up project profitability reporting, you’re flying blind. These reports can show you exactly which jobs are losing money and why—before it’s too late to fix them. Let’s break down how to create one step-by-step.

Step 1: Enable Project Tracking

QuickBooks doesn’t automatically track project-specific costs unless you enable it. Here’s how:

- Go to Settings → Navigate to

Account and Settings. - Select Advanced → Enable the

Projectsfeature. - Create a Project → Name your project and link it to a customer.

Why this matters: Without project tracking, your expenses and income end up lumped together. You’ll never know if one job is subsidizing another.

Step 2: Assign Costs Accurately

Here’s where most contractors go wrong. You need to assign every expense, invoice, and payroll entry to the correct project. Otherwise, your report will be meaningless.

Practical Example: Job Costing in Construction

Illustrative example — Let’s say you’re managing a large residential build. You’ve got material invoices, labor costs, and subcontractor bills piling up. Instead of assigning these to generic accounts like “materials” or “subcontractors,” you need to tag them to the specific project they belong to.

Pro Tip: Tools like EstimateNext simplify this step by breaking down costs into material, labor, equipment, and overhead categories. You can export these summaries and import them into QuickBooks for more detailed tracking.

Step 3: Run the Profitability Report

Once your costs and income are tagged, it’s time to pull the report. Here’s how:

- Go to Projects Tab → Select your project.

- Click on Project Reports → Choose

Project Profitability. - Filter and Customize → Add columns for income, expenses, and profit margin.

What You’ll See

The report will show:

- Income: Any invoices or payments tied to the project.

- Expenses: Labor, materials, subcontractors, and overhead.

- Profit Margin: The difference between income and expenses.

If your margin is below expectations, dig deeper. Are material costs higher than budgeted? Did labor hours exceed estimates?

Step 4: Identify Profit Leaks

Even with a profitability report in hand, you need to interpret the data. The common culprits for margin erosion include:

- Untracked Change Orders: Did the client add scope? If you didn’t account for it, your margins could shrink.

- Overtime Costs: Extra labor hours can sneak up fast.

- Material Price Changes: Did material prices spike mid-project?

General Example: Rate Adjustments

Construction firms often use standard rates for estimation. However, these rates may not account for inflation or regional price differences. Bidding on a project using outdated rates can lead to losses before the project even begins.

This is where EstimateNext can help. Their tools adjust rates to reflect current market conditions. You can upload your BOQ, get updated rates, and use them directly in QuickBooks.

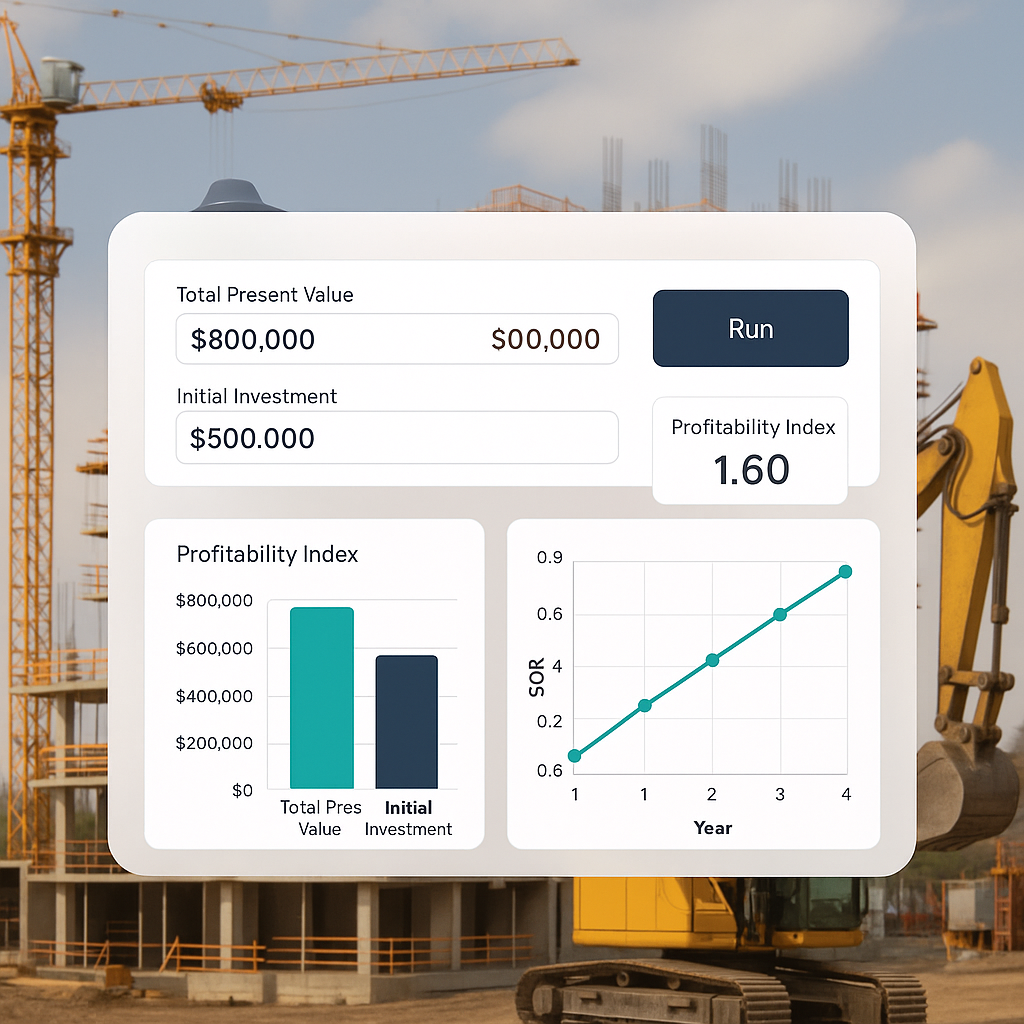

Step 5: Forecast and Plan Ahead

Profitability reports aren’t just for looking backward—they’re for planning ahead.

Example: Cash Flow Forecasting

QuickBooks lets you project future expenses based on historical data. By integrating tools like EstimateNext, you can refine these forecasts further. For instance, use their S-curve cash flow model to visualize monthly costs and income.

Common Mistakes to Avoid

- Not Tagging Costs: Forgetting to assign expenses to a project skews the data.

- Ignoring Overhead: Many contractors underestimate indirect costs like equipment rental or site utilities.

- Using Generic Rates: Standard rates are a starting point, not the final word. Adjust for inflation and location.

- Skipping Change Orders: Always track additional scope as a separate line item.

FAQ

Q1: Can I track subcontractor costs in QuickBooks Online?

Yes, you can assign subcontractor invoices to specific projects. Use the Expenses tab and tag them appropriately.

Q2: How do I handle material price fluctuations mid-project?

Update your estimates regularly. Tools like EstimateNext allow real-time rate adjustments, which you can import into QuickBooks.

Q3: Can I export profitability reports to Excel?

Absolutely. QuickBooks lets you export reports for further analysis or sharing.

Q4: Is QuickBooks enough for large-scale projects?

QuickBooks works well for basic tracking, but advanced tools like EstimateNext offer deeper insights into margins, markup, and rate analysis.

Q5: How do I calculate overhead in QuickBooks?

Create a custom cost profile that includes overhead as a percentage of direct costs. Apply this consistently across projects.

Call to Action

If you’re tired of guessing margins or relying on outdated rates, EstimateNext can help. Their tools integrate seamlessly with QuickBooks, giving you real-time cost breakdowns and profitability insights. Get started free →